Prediction markets have been reinvented many times in recent decades, from academic experiments, to corporate intelligence tools, crypto protocols, and most recently regulated financial exchanges. Each new approach promised deeper insight into human expectations, but ended up running into similar regulatory and adoption challenges. The most recent success, driven by Kalshi and Polymarket, is not just a product-design or liquidity story; it is also a regulatory story – shaped by litigation, legal interpretation, and compliance strategy as much as by user interfaces and distribution tactics.

In this first installment of our two-part series, we trace the winding path of prediction markets from their origins in the Iowa Electronic Markets to today’s multi-billion-dollar venues. We show how they have repeatedly collided with regulators, and how the parallel evolution of sports betting shaped the boundaries of what was considered permissible. Understanding this history helps frame where these markets might be headed next.

A Brief History of Prediction Markets

The Iowa Electronic Markets

The modern prediction market story begins in a bar in Iowa City in 1988. Three economists from the University of Iowa – George Neumann, Robert Forsythe, and Forrest Nelson – were complaining about how Jesse Jackson’s upset win in the Michigan Democratic caucuses had caught pollsters off guard. What if, they wondered, a market could do better? If prices in financial markets already reflected all known information about corporate prospects, maybe prices in an “election market” might better reveal the public’s expectations for political outcomes.

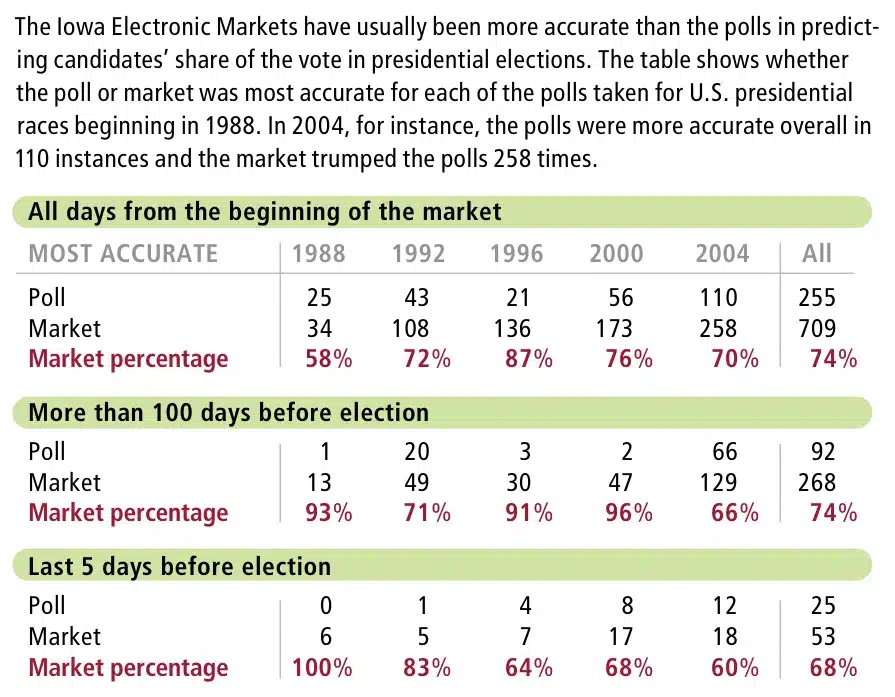

That thought experiment became the Iowa Political Stock Market, an early test of their hypothesis. Participants bought contracts that would pay out based on each candidate’s share of the popular vote. For instance, a “Bush ’88” contract would pay $0.53 if George H. W. Bush won 53 percent of the vote – a buyer at $0.50 would net $0.03 on the trade. Backed by a state attorney general’s exemption from Iowa’s gambling laws, the experiment used real money, capped at $500 per trader. When the votes were counted, the market’s closing prices predicted the final results more accurately than Gallup, Harris, or CBS/New York Times polls.

By 1992, the project had grown into the Iowa Electronic Markets (IEM), a permanent, internet-based exchange with CFTC no-action relief from the Commodity Futures Trading Commission (CFTC) as an academic research market exempt from standard derivatives regulation. This federal allowance, granted because of the small sums involved, allowed anyone with five dollars and a modem to trade. Over time, the IEM’s performance proved impressive: between 1988 and 2004, its prices outperformed traditional polls roughly three quarters of the time.

IEM’s success created a wave of imitators across industry, government, and finance. By the late 1990s, researchers and policymakers were exploring whether similar market mechanisms could help aggregate intelligence in other domains, including disease outbreaks, while corporates such as Hewlett-Packard and Google launched internal markets to predict product-launch timelines.

In 2003, the Defense Advanced Research Projects Agency (DARPA) worked with George Mason professor Robin Hanson on the Policy Analysis Market, a Pentagon-sponsored exchange that would enable traders to bet on geopolitical events such as coups, terrorist attacks, or regime changes. This project was met with firm bipartisan opposition – with Senator Barbara Boxer of California famously stating “There is something very sick about it”. Altogether, however, it was probably the most consequential effort in getting the public at large (including future entrepreneurs) to care about prediction markets. In the words of Joyce Berg, a professor of accounting and the IEM’s interim director: “It actually took the DARPA thing to get people’s attention”.

Initial commercial attempts and an evolving regulatory framework

Commercial attempts soon followed. In the early 2000s companies such as HedgeStreet (which evolved into the North American Derivatives Exchange or NADEX) attempted to list event contracts under U.S. derivatives law. In 2004, HedgeStreet was designated the first contract market dedicated to event contracts by the CFTC. Yet, even as these markets expanded, their legal foundation remained ambiguous. In May 2008, the CFTC published its Concept Release on the Appropriate Regulatory Treatment of Event Contracts, a 24-question consultation on whether event contracts were legitimate derivatives, gambling instruments, or something in between. The CFTC explicitly asked whether these products served a public interest through hedging or price discovery, and how to distinguish between informational and gaming contracts. While they fell short of creating a definitive framework, partly due to the 2008 financial crisis, these questions significantly shaped regulatory discussions for the next decade.

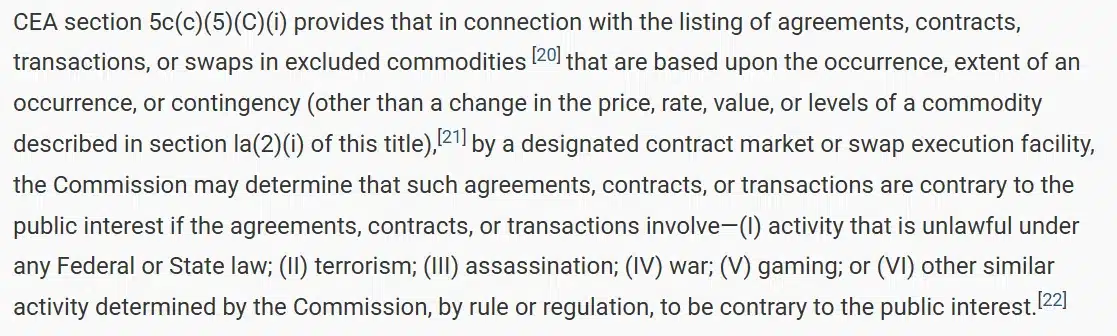

In 2010, Congress codified the CFTC’s jurisdiction over event markets through Section 745(b) of the Dodd-Frank Act, which added Section 5c(c)(5)(C) to the Commodity Exchange Act (CEA). The new provision empowered the CFTC to prohibit contracts deemed “contrary to the public interest” explicitly naming five restricted categories: terrorism, assassination, war, unlawful activity, and gaming. One year later, the CFTC implemented Rule 40.11, formalizing that mandate: any exchange that listed a contract related to those subjects would be subject to review and possibly denial.

From there, a familiar pattern emerged. Companies would launch event markets, attract some early user enthusiasm, and then run into regulatory bottlenecks. NADEX, for example, was allowed to list binary options on economic data but blocked from offering political or sports contracts. In 2012, the CFTC rejected NADEX’s filing for election futures on a “gaming” basis citing failure to meet the economic-purpose test – the standard requiring that a contract support hedging of a commercial risk or support price discovery. That rejection set an important precedent: event contracts involving political or sports outcomes would be categorized as “gaming” unless proven otherwise.

Prediction markets move overseas

With U.S. operators constrained, foreign markets briefly filled the gap. Intrade, based in Dublin, became the global face of prediction markets in the early 2010s, offering contracts on elections, geopolitics, and even celebrity news. At its peak, Intrade prices were quoted by CNN and The New York Times as quasi-forecasts of political races.

In 2013, however, U.S. regulators charged Intrade with illegally serving American customers without registration, and it shut down soon after. The only US holdout was PredictIt, operated under a CFTC no-action letter granted to Victoria University of Wellington. This exemption allowed real-money political trading within strict limits ($850 per contract and a nonprofit research mandate), effectively preserving the IEM’s academic spirit without scalability[1].

By the 2010s, the regulatory stance had hardened. Under Section 5(c) and Rule 40.11, the CFTC was both authorized and inclined to interpret the term “gaming” broadly. Contracts on elections, sports, or human conflict were presumptively barred. What began as a gray area had become a red line.

Crypto’s early attempts

The next attempt to revive prediction markets came from the crypto world. Blockchain entrepreneurs viewed decentralization as a way to get around the regulatory choke points that had thwarted prior generations. If the CFTC treated event contracts as off-limits for centralized intermediaries, then the answer, in their view, was to eliminate the intermediary from the equation entirely.

One major project that aimed to realize this idea was Augur, launched in 2018 on Ethereum. Augur was conceived by a group of developers, economists, and early crypto idealists – including Joey Krug and Jack Peterson – who saw smart contracts as a way to create markets for truth. On Augur, any user could create a market on any event, post collateral, and rely on “oracles” (users who reported outcomes) to settle the results. In theory, this was the prediction market freed from regulatory burden. In practice, Augur never really took off. Thin liquidity, complex interfaces, slow settlements, and expensive gas fees prevented the platform from offering the experience it set out to create.

The winding paths of Kalshi and Polymarket

Around the same time, Kalshi and Polymarket got their start.

Kalshi was founded in 2018 by Tarek Mansour and Luana Lopes Lara with the goal of building the first CFTC-regulated exchange dedicated entirely to event contracts. In 2020, it became the first new Designated Contract Market (DCM) in nearly a decade. This early regulatory blessing, however, did not translate into traction. In its first two years of operation, Kalshi’s volumes were unremarkable – on the order of a few thousand contracts per day, often concentrated around one or two macroeconomic events such as Federal Reserve decisions or monthly inflation prints. Retail users found the topics narrow, while institutional players saw little hedging utility in them.

Despite this slow start, Kalshi persisted, expanding its product lineup to include contracts on consumer sentiment, GDP growth, and unemployment figures. It began lobbying for broader contract categories with a better chance of attracting meaningful volume. Its founders then began to argue that the most pressing “real-world risk” Americans face is not CPI volatility but political and policy uncertainty; in 2023, Kalshi decided to test this thesis directly.

That year, Kalshi filed to list contracts on which party would control Congress after the 2024 elections, framing them as hedges against policy risk. The CFTC rejected the contracts under Rule 40.11 and Section 5(c)(5)(C), classifying them as unlawful “gaming.” Kalshi sued, arguing that the CFTC had drawn an arbitrary line between political risk and every other form of market risk. In September 2024, a federal district court sided with Kalshi, ruling that the CFTC had overstepped its authority and that the contracts were permissible under the CEA. Kalshi then listed contracts on that year’s presidential election and saw its first real spark of widespread interest. The CFTC appealed but ultimately dropped the case in May 2025, possibly as a result of the changing regulatory posture of the new administration. That decision left the district court ruling intact and removed the immediate federal barrier to exchange-listed political event contracts.

Polymarket, by contrast, came from the opposite direction: a crypto-native platform that began life as the anti-Kalshi; borderless and decentralized. Launched in 2020, it enabled users to trade yes/no tokens on everything from election results to COVID case counts, settling in stablecoins. At its 2021 peak, Polymarket hosted over $100 million in open bets and became the most liquid prediction market in the world.

In January 2022, however, the CFTC fined Polymarket $1.4 million for operating an unregistered exchange and ordered it to block U.S. users. For the next three years, Polymarket continued to see steady growth – with a notable election spike surpassing Kalshi’s – while also moving toward compliance and courting institutional investors. In July 2025, Polymarket announced its return to the U.S. market through the acquisition of a CFTC-licensed exchange and clearinghouse, effectively marking its evolution into a regulated derivatives venue.

The Shifting Sports Betting Regime

Daily fantasy sports

While prediction markets were on their wandering commercial and regulatory journey, sports markets were progressing along a parallel path. For most of the modern era, federal law treated sports wagering as a threat to the population’s integrity. The Professional and Amateur Sports Protection Act (PASPA) of 1992 prohibited new states from authorizing betting on professional or amateur sports, effectively confining legal wagering to Nevada.

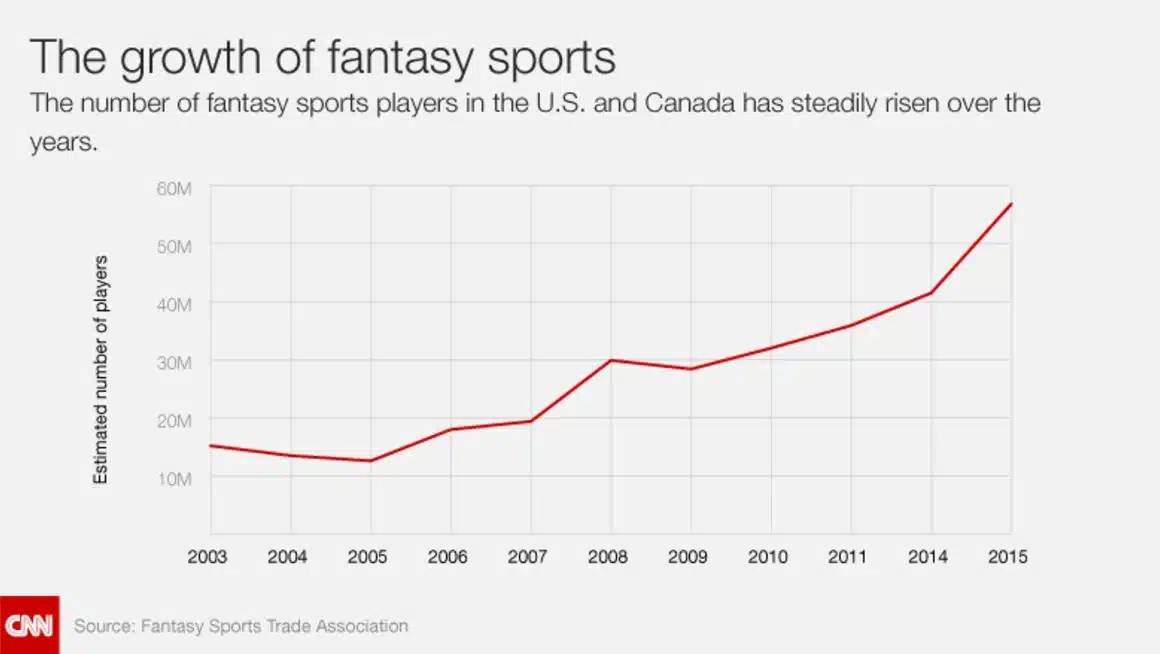

That landscape began to shift in 2006, when the Unlawful Internet Gambling Enforcement Act (UIGEA) included an exception for fantasy sports. This carve-out allowed contests that (i) spanned multiple real-world games, (ii) were determined mainly by skill rather than chance, (iii) offered fixed prizes, and (iv) avoided reliance on a single player or match outcome. This language, originally intended to protect casual season-long fantasy leagues, became the legal foundation for daily fantasy sports (DFS) operators.

Throughout the 2010s, DFS platforms grew rapidly under this exemption. They marketed themselves as games of skill, not gambling, and as a result faced lighter regulatory oversight than traditional sportsbooks.

Today, these companies (most famously DraftKings and FanDuel, but also the likes of PrizePicks, Underdog, and JockMkt) continue to operate in more than 40 states under the same framework. Some states have moved to restrict or reclassify them, but the general model persists.

PASPA strike down – state sanctioned gambling advances

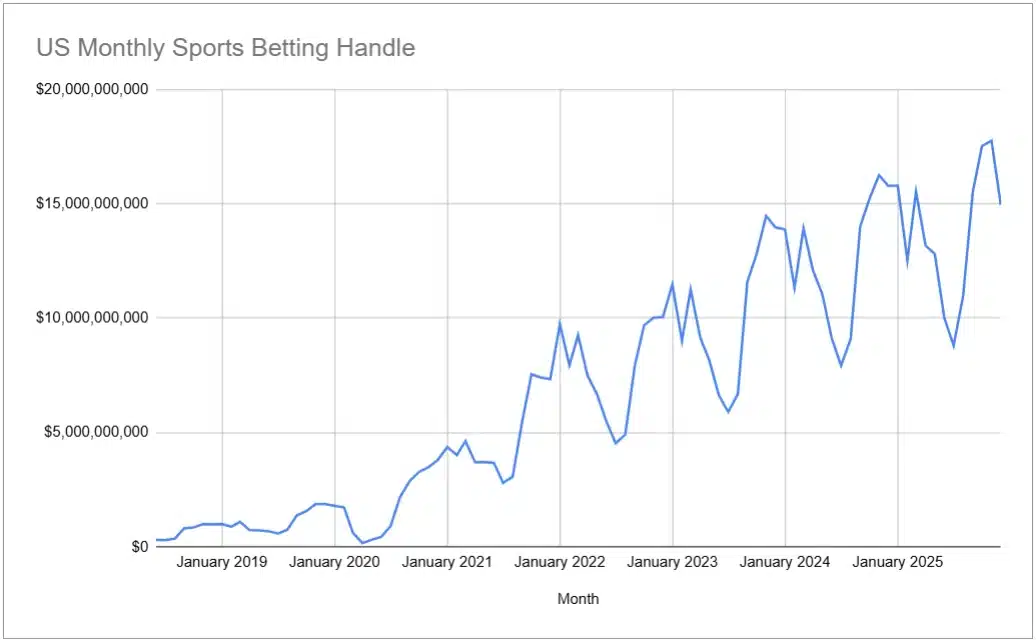

The full prohibition on traditional sports betting ended in 2018 when the Supreme Court’s Murphy v. NCAA decision struck down PASPA as unconstitutional. Since then, individual states have been allowed to make their own decisions; roughly 37 states and Washington, D.C. have legalized some form of wagering and the industry has taken off.

Americans wagered an estimated $165 billion on sports in 2025, and the total handle since legalization has already surpassed half a trillion dollars. Sportsbook promotions are now fixtures of professional sports broadcasts, team sponsorships, and even in-arena experiences.

Ironically, the companies best positioned to capitalize on legalization weren’t the legacy casino operators, but the DFS platforms. DraftKings and FanDuel, which built massive user bases under the fantasy-sports exemption, pivoted almost overnight into sportsbooks. Their technology, data infrastructure, and customer funnels were already in place; all they were missing was a legal framework. When states began authorizing mobile wagering, DraftKings and FanDuel were first in line, quickly joined by BetMGM, Caesars, and a handful of regional operators.

But the growth story masks a series of structural challenges. Under current gambling laws, each state requires its own license, its own compliance stack, and often a local casino partner. Entry fees can be large – New York, for example, charges a $25 million one-time licensing fee and taxes gross gaming revenue at 51 percent. Smaller operators have struggled to break in; many that launched after the PASPA repeal have since consolidated or folded. The market has effectively coalesced around a handful of dominant players who can afford the regulatory overhead and customer acquisition costs.

Adding to the regulatory complexity is the 1961 Wire Act, which prohibits wagers transmitted across state lines. As a result, each state functions as a self-contained sports betting market with its own liquidity pool and pricing dynamics. Odds on the same game can vary by geography, and consumers in one jurisdiction can’t access the liquidity of another. What exists today is not a national marketplace but dozens of small ones, stitched together by a few national brands.

Prediction markets meet sports betting

For years, the CFTC framework around “gaming” effectively shut the door on sports. In 2020 ErisX, a CFTC-regulated exchange better known for crypto derivatives, filed to list NFL moneyline and point-spread futures. The contracts were simple binary payoffs – $100 if a team won, $0 if not – but the regulatory logic behind them was new. ErisX argued they would enable sportsbooks to hedge one-sided exposure, such as when local bias led most bettors to favor the home team. The CFTC halted the filing under Rule 40.11, and ErisX withdrew before a formal vote.

However, two CFTC commissioners published opinions that proved consequential. Commissioner Brian Quintenz dissented from the rejection, calling the CFTC’s treatment of “gaming” overly broad and arguing that post-PASPA legalization meant such contracts were not inherently contrary to the public interest. Commissioner Dan Berkovitz, while opposing the contracts, acknowledged that sports wagers could serve legitimate economic purposes if designed correctly, suggesting that an exchange listing sports futures open to retail participation with identified hedgers might eventually meet the statutory test. Those statements marked the first openings in a previously solid regulatory wall.

The CFTC then tried to draw brighter lines. In May 2024 it issued a Notice of Proposed Rulemaking to amend Rule 40.11, proposing that event contracts involving the enumerated activities, including “gaming” defined to encompass athletic contests and political contests, be deemed per se contrary to the public interest. Two commissioners dissented, warning against categorical bans and urging a case-by-case standard.

Then came a pivotal moment for the industry: in early 2025, Kalshi officially began listing self-certified sports-related contracts. This launch shifted the landscape, forcing a theoretical regulatory debate into a live-market reality. In response, the CFTC pivoted to a posture of reconsideration rather than outright prohibition. In February 2025, shortly after Kalshi’s launch, the agency announced a Prediction Markets Roundtable to gather stakeholder input on sports-related event contracts and broader informational markets. By September, CFTC staff issued an advisory addressing “exchange-listed sports event contracts” signaling that regulated futures markets could be legitimately evaluated under current rules, even if none have yet been approved. The advisory clarified expectations around access, clearing, and risk-mitigation.

Meanwhile the Notice of Proposed Rulemaking remained under review: although the comment period closed on August 8, 2024, the CFTC had not yet adopted a final rule. For a brief period in late 2025, the status was hybrid: official rulemaking was paused, staff guidance was emerging, and individual contract filings (especially by smaller DCMs) were under active review rather than being categorically banned.

That hybrid status, however, came to an end in early 2026. Under the leadership of newly confirmed CFTC Chairman Michael S. Selig, the agency shifted from a pause in rulemaking toward more active engagement on the jurisdictional treatment of event contracts. On February 4, 2026, the CFTC officially withdrew the lingering 2024 Notice of Proposed Rulemaking, withdrawing the proposal that would have deemed certain sports and political event contracts per se contrary to the public interest under Rule 40.11. This was accompanied by the staff’s withdrawal of its advisory.

Rather than leaving platforms to navigate a regulatory gray area, the CFTC has now articulated a clearer jurisdictional position. In a flurry of early 2026 legal activity, the agency began filing amicus briefs in federal appellate courts, asserting that event contracts on designated markets are derivatives subject to the Commodity Exchange Act’s federal regulatory framework and the CFTC’s primary jurisdiction. This interpretation argues that the Commodity Exchange Act significantly limits the extent to which states may regulate federally designated derivatives exchanges as traditional sports betting operators. As a result, the market’s regulatory battleground has shifted: the core question is less about categorical federal prohibition and more about whether federal courts will uphold the agency’s jurisdictional position in response to a growing number of state-level enforcement actions and legal challenges in places such as Nevada, Tennessee, and Massachusetts.

The State of Prediction Markets Today

As their regulatory journey has converged with that of sports betting, prediction markets have taken off. Over the past two years, Polymarket and Kalshi have seen astounding growth from barely any trading activity to weeks in the billions of notional traded.

These markets are dominated by the two categories of contracts that have sparked the fiercest debate over decades of regulation: elections and sports. Elections drove the first peak in November of 2024, while sports have dominated since. For Kalshi in particular, the share of monthly sports-driven volume has frequently been in the 90% range.

Elections contracts appear to have clear regulatory grounding for now yet bring the major downside of being incredibly infrequent. Sports contracts, on the other hand, have great recurrence properties (notwithstanding some seasonality) but are on very unclear regulatory grounding. This leaves today’s prediction markets in a somewhat fragile position, despite their extraordinary growth.

In the next installment of this series, we will take a closer look at the activity on prediction markets to date and the infrastructure gaps that must be addressed for these markets to reach their full potential.

If you are interested in this and/or working on something in the prediction market space, please reach out to us at ventures@tower-research.com, pdecio@tower-research.com or nbaronia@tower-research.com.

The views expressed herein are solely the views of the author(s), are as of the date they were originally posted, and are not necessarily the views of Tower Research Ventures LLC, or any of its affiliates. They are not intended to provide, and should not be relied upon for, investment advice, nor is any information herein any offer to buy or sell any security or intended as the basis for the purchase or sale of any investment. The information herein has not been and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date of preparation. Certain information contained herein is based on published and unpublished sources. The information has not been independently verified by TRV or its representatives, and the accuracy or completeness of such information is not guaranteed. Your linking to or use of any third-party websites is at your own risk. Tower Research Ventures disclaims any responsibility for the products or services offered or the information contained on any third-party websites.

[1] The CFTC revoked that relief in 2022. PredictIt sued, and the case was recently resolved in PredictIt’s favor.