In our previous article, we covered the long and tumultuous history of modern prediction markets from 1988 to the present day, including leading prediction marketplaces like Kalshi and Polymarket. Today, we’ll examine the bull and bear cases for the sector in 2026. Overall, we see an opaque regulatory cloud hanging over this space, with open questions on the durability of today’s platforms. However, the growth, momentum, and opportunities for vertical integration mean it must be monitored carefully.

In this piece, we will cover open areas for product exploration and mechanism design that we think will drive the future of prediction markets. Today many prediction markets focus on capturing value from retail participants – we believe other participants have been underserved. For sophisticated traders, we anticipate better financial products to give them leverage and improve capital efficiency; for hedgers, we anticipate ways to monetize their implicit interest in true-price discovery mechanisms. And, we still see growth for retail traders – we anticipate experiences evolving towards entertainment and media, rather than towards purely betting.

Prediction Markets Today

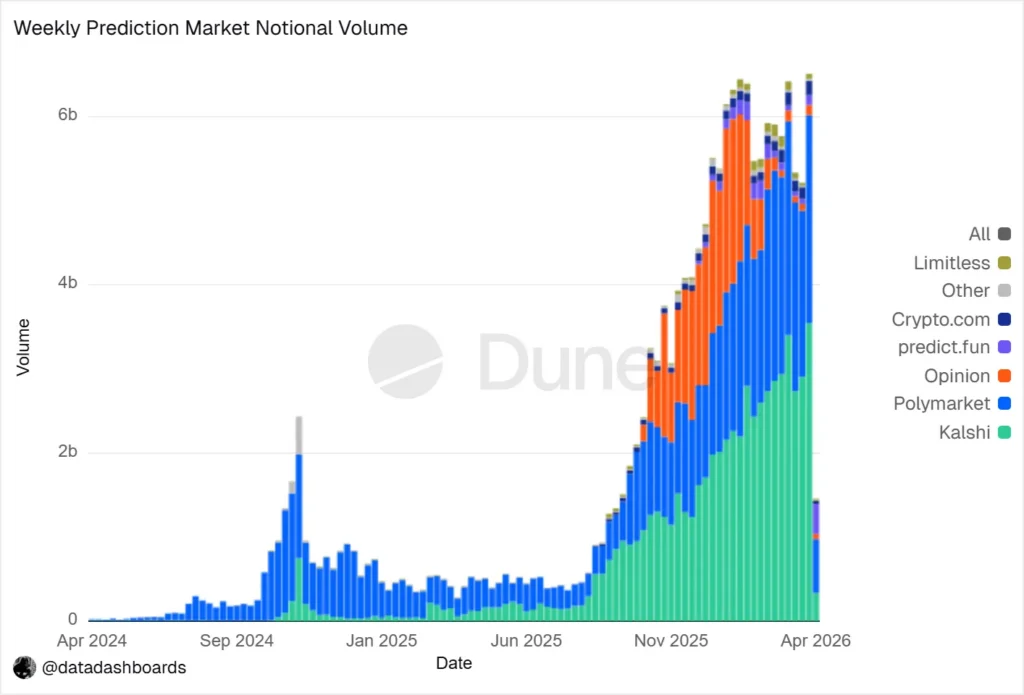

Prediction markets may have lurched forward in fits and starts, but by simply glancing at their trading volumes it appears 2025 was the year they achieved lift, with annualized volumes exceeding $40B for the leading players.

Vertiginous growth like this is hard to ignore – before the present boom, weekly volume had peaked at $2.4B in late 2024 around the U.S. presidential election, and now the major players are doing upwards of $6B a week in early 2026. Understandably, investors have taken notice. Their attention is not just on trading via these platforms, but on the platforms themselves. If you put on your ZIRP goggles the vision is fairly clear: they can create markets on everything and enable users to hedge anything, effectively functioning as financial truth machines. It’s NYSE, scaled to a much wider set of topics and risks. However, the narrative and hype seem to have diverged from reality in both direction and magnitude.

Current Constraints on Prediction Market Companies

As covered in our last installment, prediction markets businesses inherit a long history and context of market opportunity and regulation. They may be structurally narrower, more retail-dependent, and more liquidity-constrained than the hype suggests. Let’s consider a few of these headwinds before we consider the corresponding tailwinds.

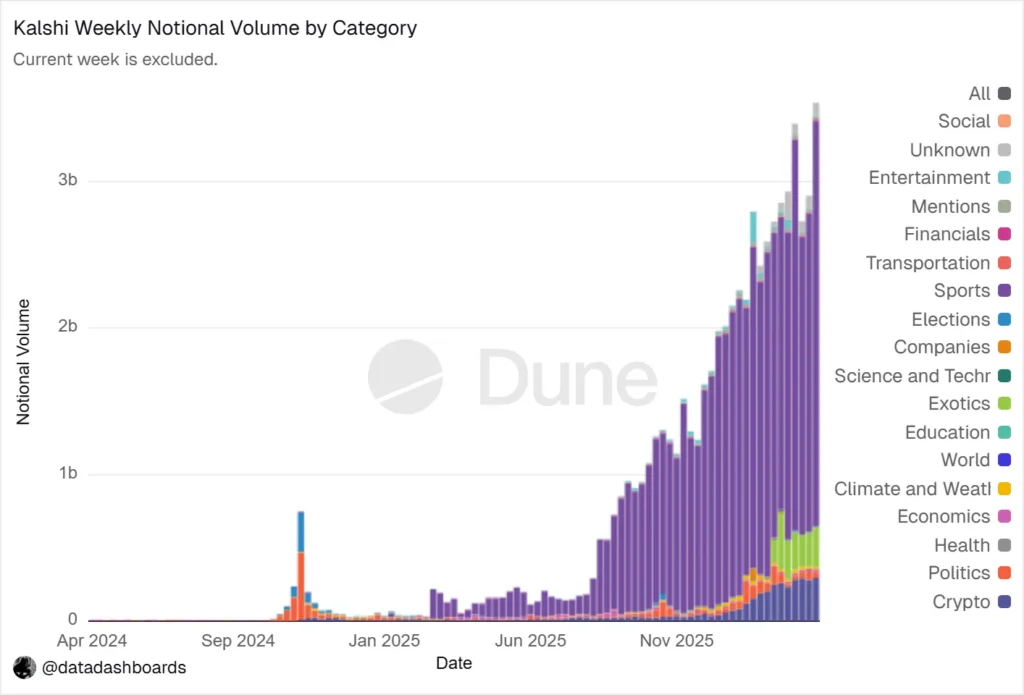

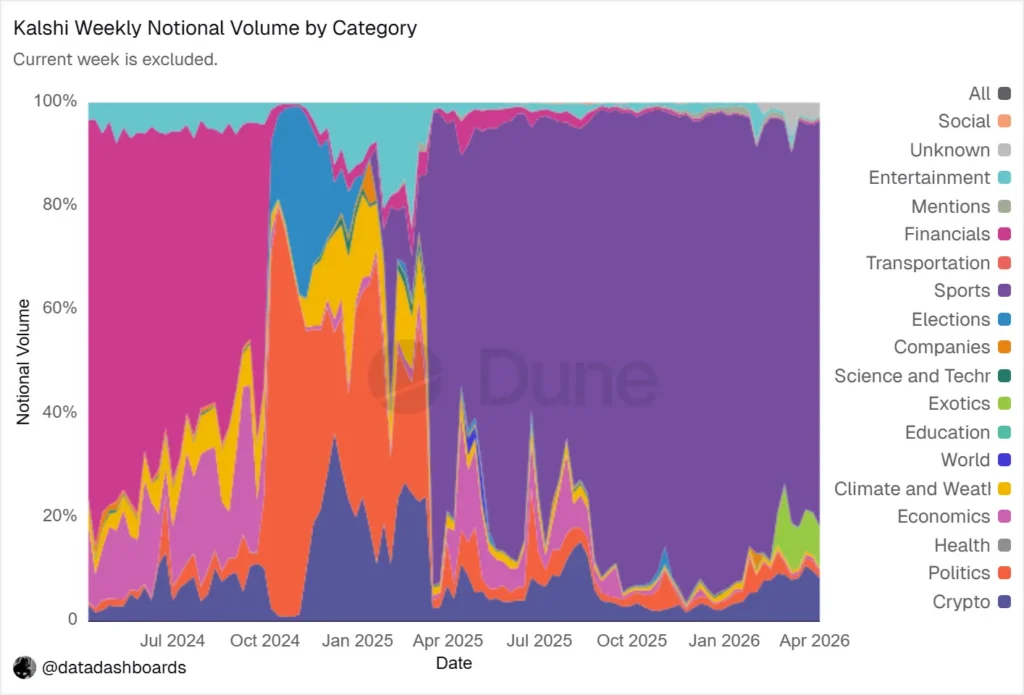

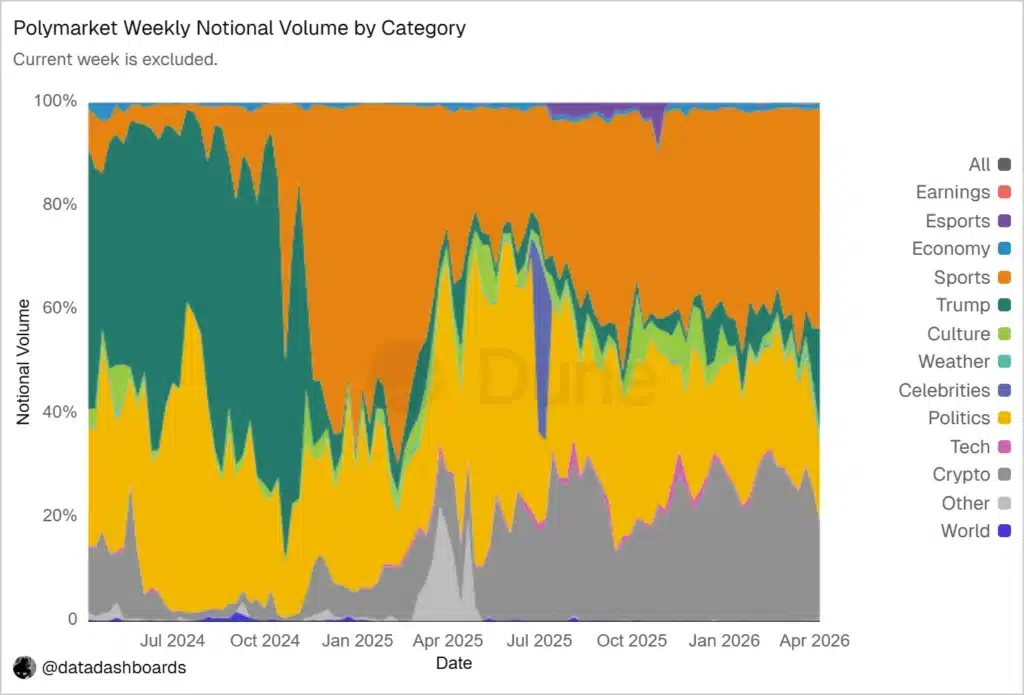

Category Concentration

While largely positioned as “markets for anything,” prediction markets are in practice servicing one very specific market: sports betting. Per Kalshi’s volume & category blend:

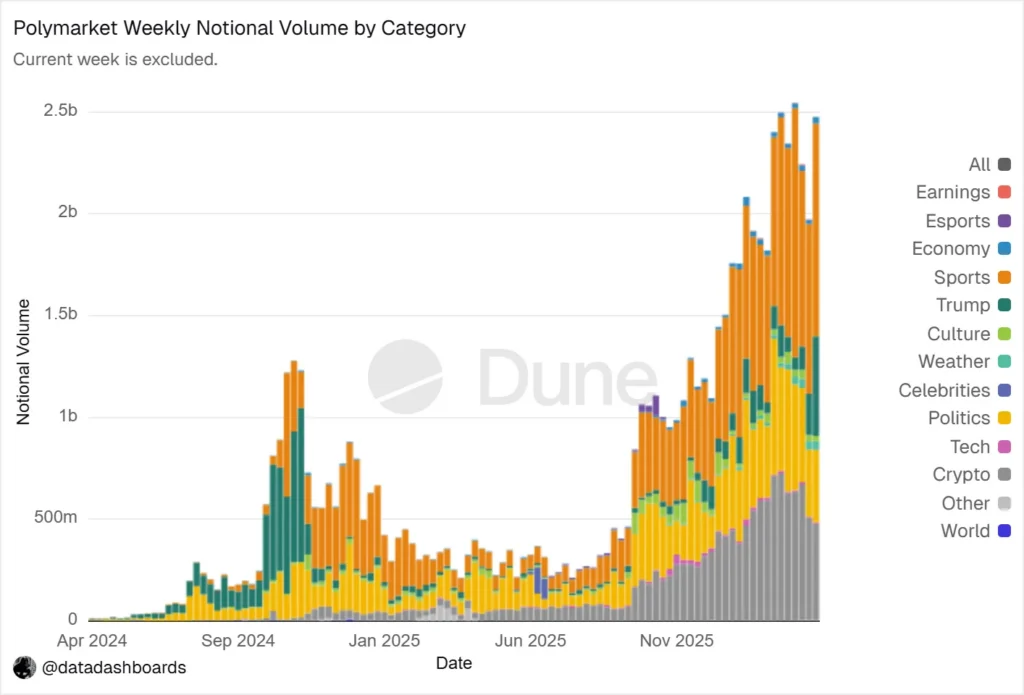

The overwhelming majority of Kalshi’s $3B weekly activity comes purely from sports contracts (~80%). Polymarket sees similar weekly activity, which has a slightly more diverse blend:

Close to 40% of Polymarket’s volume is sports. Another 33% is crypto, while around 20% is political events.

In effect, we still don’t really have prediction markets in the way people have been pitching. We have largely concentrated, sports-betting venues that also occasionally allow betting on crypto prices, politics and underground ancient Egyptian power generation. The core premise of prediction markets as oracles for a long tail of specific events still doesn’t appear to have found PMF, either with retail traders or with farmers looking to hedge the weather.

A Restricted and Competitive Market

While new prediction markets may be growing in large part due to sports betting, sports betting itself isn’t exactly a greenfield area. Regional casinos have been servicing this market for decades, and online players like FanDuel and DraftKings have been around since 2009 and 2012, respectively. In general, sports betting has always been considered a local gaming issue, which means its legality and the oversight of its participants is usually dealt with on a state-by-state level. This is a key part of the moat of the incumbent sports betting platforms: over years, they assembled a state-by-state patchwork of licenses that let them operate across most of the country – licenses that prediction market entrants argue they don’t need. Kalshi claims it already has the relevant national licenses (including Designated Contract Market and, through its affiliate, Derivatives Clearing Organization licenses from the CFTC), and previously sued the CFTC arguing that contracts on US election outcomes should be treated as federally regulated derivatives rather than state-regulated gambling products. While Kalshi has been permitted to list certain election-related contracts, the broader regulatory treatment of event contracts (particularly those tied to sports) remains unsettled at the federal level.

Furthermore, states have already begun to take action insisting that they have the correct jurisdiction over these products, with Nevada recently issuing a Temporary Restraining Order on Kalshi (to be discussed at a hearing in April). Additionally, Arizona’s Attorney General Kris Mayes recently filed criminal charges against Kalshi alleging violations of state gambling and election laws. Per Mayes’ press release:

“Kalshi may brand itself as a ‘prediction market,’ but what it’s actually doing is running an illegal gambling operation and taking bets on Arizona elections, both of which violate Arizona law. No company gets to decide for itself which laws to follow… Arizona will not be bullied into letting any company place itself above state law.”

As states attempt to bring the regulatory jurisdiction for prediction markets down from a national level to a state one, established sports-betting businesses are positioning themselves to take advantage of a national jurisdiction for sports-betting, should federal courts side with the upstarts. Per Peter Jackson’s (CEO of Flutter Entertainment, parent company of FanDuel) 2025 Q3 earnings call, “The sports prediction market opportunity lies solely in those states currently without sports betting access, as we can clearly see prediction markets are having a negligible impact in the states where FanDuel Sportsbook is already available to customers. The opportunity to extend the FanDuel footprint into these new states is significant…” He views this rapid market growth largely as a form of regulatory arbitrage, and insofar as that arbitrage settles on the side of prediction markets, the incumbents intend on competing.

Even if prediction markets do secure a regulatory opening, however, the next question is whether they can sustain deep, durable participation. Capturing and retaining retail trading or gambling is quite expensive.

Competing for Retail Attention

Similar to retail brokerages or retail banking, a lower CAC or better LTV will become critical to prediction markets establishing dominant market share amongst retail traders. Draftkings and Flutter do not directly disclose exact CAC/LTV metrics, but Draftkings’ FY 2024 statements imply a CAC of ~$300, while Flutter estimates payback periods to be ~18mo. In both cases, sales and marketing represents the largest single expense for these companies outside of raw costs of sales (payment processing, taxes, revshares, etc.), and can amount to 25% – 30%+ of revenue.

We don’t currently know the CAC or LTV for Kalshi or Polymarket, but we can use their public sports betting counterparts’ metrics as guideposts to consider where the majority of their costs might be going forward. Furthermore, since Kalshi and Polymarket do not operate like traditional sports books, their take rate is much narrower than the incumbents – DraftKings’ Net Revenue Margin (their ‘hold’/take rate on the full ‘handle’/volume bet, less promotions and free bets) hovers around 6.0%, while FanDuel’s hovers around 8.6%. By comparison, Kalshi has a variable trade fee that averages in the 1%-2% range, and Polymarket’s fees cap out under 2%. In effect, this means that as prediction markets continue competing head-to-head with established sports-betting platforms, they will have to facilitate far more volume to earn comparable net revenues to reinvest into user acquisition.

This problem multiplies as other large financial firms begin to elbow into sports betting – already Robinhood (which uses Kalshi as its DCM – more on that in a moment) is reportedly originating the majority of Kalshi’s volume, while also maintaining its own plans to enter the DCM business in Q2 of 2026, via its acquisition of MIAXdx.

A Lack of “Natural” Buyers and Sellers

Many large asset classes include some inherent value creation, enabling types of participants who aren’t solely interested in collecting mispricings. We can call these participants “natural” buyers and sellers – businesses may need to raise capital via equity or credit (making them natural sellers) while savers (banks or investment funds) may want to provide capital via equity or credit (making them natural buyers). Even in commodities, which do not naturally produce cash flows, there are natural sellers (like farmers or oil producers) and buyers (like restaurants or transportation companies) of the underlying asset without having to tap into speculators or hedgers.

Across these asset types, multiple parties can be better off with the same trade, which isn’t true out of the box with prediction markets. In prediction markets, the incentives are the same – namely collecting some expected mispricing. There is no underlying economic transaction, which severely reduces the population of potential counterparties for a given trade. In the case of prediction markets the reduced set of counterparties, as mentioned by Nick Whitaker and J. Zachary Mazlish’s “Why Prediction Markets Aren’t Popular”, are “sharps” (participants who “enter markets to profit from superior analysis”), retail traders (referred to in the article as “gamblers”), and occasional hedgers.

To take a simple example, suppose there is a contract paying $1 if Jesus Christ returns before 2027. A sharp could buy at 4 cents because they think the true probability is 10 cents. But in this case, who is the seller for this? For many contract types, it’s not evident that there is some company or pension fund urgently interested in shorting this contract for business reasons. And other than the sharp, who is the buyer for this, other than retail speculators? Most event contracts lack interest from parties other than sharps, which means the open interest stays small, volume stays low, and spreads stay wide.

Kalshi and Polymarket have launched more traditional event contracts encompassing macroeconomic data and index activity that could feasibly be useful to traders who already look for these instruments (“Will the S&P 500 close between 8,000 and 8,200 this year?”). While the comparative contract simplicity may favor retail traders (a 5 cent contract implying a 5% chance, rather than a complex call spread with a premium), institutional traders don’t seem to have jumped in meaningfully. Per a recent Bloomberg article, “Since late December, Kalshi users have traded over $1 million in bets on where the S&P 500 will end the year. On the options market, more than $100 million of notional volume trades every day in S&P 500 contracts that expire on Dec. 31.” While prediction markets offer traditional financial event contracts, they don’t seem to be drawing activity, either from institutions or retail traders.

Per the category blend charts of Polymarket and Kalshi shown above in the “Category Concentration” section, the dominant category for trading is sports betting (and to a lesser extent, crypto and politics), which has limited appeal for market participants outside of retail traders, and the sharps who can price probabilities more efficiently than retail. Later on, we’ll explore how (if at all) prediction markets’ mechanisms can be designed to be positive-sum or value-creating, but as of today most user personas can employ their capital in other more attractive assets.

Moats and Catalysts for Prediction Market Companies

Despite the critiques we lay out above, there are still reasons to be excited by what prediction market companies have built so far.

Vertical Integration

In many financial markets, businesses tend to stratify and specialize, with distinct players operating at the broker layer (what software investors might call the “app layer”), the exchange layer (what software investors might call the “marketplace layer”), and the settlement and clearing layer (what software investors might call the “system of record layer”). Kalshi and Polymarket are highly unique in that they have built out offerings at every layer of the stack, operating consumer brands on the broker/app level down and exchanges and regulated clearing services on the settlement level. Many of their larger competitors on one level of the stack become partners or customers on another. Robinhood, for example, is an FCM but not a DCM – they route their trades to Kalshi’s DCM, which can also be traded on from Kalshi’s frontend (or another third party). Similarly, Polymarket has bought and built out clearing capabilities, which are now used by their competitor DraftKings.

Regulatory Arbitrage

As discussed, much of the current prediction market strategy seems to hinge not only on assuming that CFTC-regulated derivatives frameworks may preempt or limit the applicability of state-by-state gambling regimes, but also that prediction markets players have free rein to operate prior to any official federal ruling. Although this approach could be called regulatory arbitrage, advocates and investors in prediction markets would argue many now-dominant and acceptable startups began with regulatory arbitrage. Popular sharing/gig economy companies violated laws, and the law eventually changed. For example, in Oct 2010 the California Consumer Protection & Safety Division issued a cease-and-desist against Uber for “advertising and operating as a passenger carrier for hire without Commission authorization”, but by Sept 2013 the governing California Public Utilities Commission explicitly created a new regulatory category (called Transportation Network Companies) to allow Uber and others to continue operating.

The altruistic view of these platforms (and their recent investors) is that they believe current rules and regulations are anachronistic, and that they can either outlast a hostile regulatory regime or can actively shape the regulatory regime they will operate in down the road.

So What Should Be Built?

Tools for Pros

One underserved market within sports betting is the professional and semi-professional bettor. Today, prediction market UIs are optimized for retail simplicity. Their counterparts, the sports books, are not designed to support large amounts of professional bets. This leaves the entire persona segment untouched, and ripe for startups. We see opportunities for prediction markets and startups to launch tools similar to sophisticated investing tools in traditional markets – this could amount to new UIs for multihoming across platforms (Axiom has shown success with its highly sophisticated trading platform), infrastructure for automated trading, or post-trade/back office tooling.

Prediction markets also allow users to trade automatically, whereas users on sportsbooks are limited from placing bets non-manually. Prediction market tools that hinge on that difference will be successful if sports contracts are here to stay. API-forward tools (data feeds, trade routing, etc.) should exist in similar form to analogous products in traditional financial markets. For example, Nasdaq generates about as much revenue from its Market Services unit (trading operations) as it does from its Capital Access Platforms (market data feeds, listing fees, index licenses) and Financial Technology (regulatory and financial crime SaaS tools) business lines. In theory, markets have more in common with traditional exchanges than to sportsbooks; they too can explore these other business lines beyond taxing the traders directly.

Importantly, as more and more types of prediction markets exchanges and brokers enter the market, aggregate tooling for pre-trade and post-trade work becomes more necessary. Sports-books are unincentivized to build these things, since they don’t want to cater to sophisticated traders to begin with, and sophisticated traders are likely to multi-home across the major venues, making first-party tools for pros less relevant. We anticipate that the breakout professional products will be built by prediction markets traders who feel this pain themselves.

Creative Forms of Leverage

For larger traders to meaningfully trade they usually need some ability to both finance and net their positions within a given venue and across different venues. Existing brokers either do not want to or have not yet emerged to provide leverage.

Prediction markets are unique in their binary settlement in a vast array of uncorrelated markets, oftentimes with no historical precedent. This makes it difficult for generalist capital providers to provide leverage and monitor counterparty liquidity. Certain entrepreneurial prime brokers like Clear Street and Marex have already started offering liquidity and trading capital to institutional clients, though these offerings do not yet extend to all event contracts on these markets. Against the backdrop of rising institutional interest and activity in prediction markets, we could see new-age prime brokers emerge, purpose-built for prediction market traders.

Sophisticated brokers and clearinghouses already provide variations of Risk Based Margin Financing – in effect this means a financier can take into account all of a trader’s positions and come up with volatility estimates for each asset as well as the specific basket. As an example, a lender might be comfortable with lending for trading on the next U.S. presidential election due to its liquidity, with the provision that it refuses to lend in the week leading up to the event (limiting the chance that the financed position gets wiped out in a jump).

While RBMF already exists with many brokers, this usually requires some nuanced pricing and understanding of the specific asset class. This X thread by Messari Research covers a few financing examples that are unique to prediction markets.

Existing platforms like Kalshi or Polymarket likely don’t want to be in the business of extending credit to their users, and existing prime brokers may not fully appreciate the risk/reward tradeoff of building a lending business in this category, giving startups ample space to experiment and grow.

Monetizing Information Externalities

With many other forms of markets (equity, credit, etc.), a participant can both create value and capture that value. The overall economic pie can become larger, and that economic expansion can be monetized in some way (as well as traded around). In a player-versus-player event contract, the resolution of the event and the transfer of capital from one account to another does not itself generate any new economic value. Every gain has to be offset by someone else’s loss.

Regardless of how much value is directly extracted from the traders in a prediction market, there is another source of economic value that merits monetization, which is the value of the information revealed by the market. For example, a recent Federal Reserve study found Kalshi’s events on macroeconomic forecasts to be:

“Well-behaved, responsive to news, and comparable in forecasting accuracy to established benchmarks such as the Survey of Market Expectations and the Bloomberg consensus. In several cases, they provide unique insights—particularly for variables like GDP growth, core inflation, unemployment, and payrolls, for which no other market-based distributions currently exist. We have also argued that they provide the only credible measures of distributional beliefs about decisions at specific FOMC meetings.”

These event contracts themselves are very thin, with less than $100k of total volume traded for many of them, but the forecasting accuracy for policy makers and researchers is incalculably more valuable. Prediction markets should look at ways to price and capture this implicit and unique value. Per a 2012 paper, an entity seeking information (“Will the opening day box office for my movie be X?” or “Will next year’s defense budget be less than Y?”) can choose to directly subsidize the generation of this information, via either a direct bounty or “Bayesian Market Making”. The particular method of subsidy is less important than the main idea: entities can stimulate event contracts on things they specifically find interesting ex ante, rather than looking at existing contracts to see what could be useful ex post.

To be clear, monetizing these types of externalities is not impossible for the major prediction markets, though none have yet taken any steps to do so. Startups will need to have a strong point of view on why they can not only find and monetize the people behind these positive externalities, but also construct some way to retain them.

Markets as Entertainment & Media

Another ambiguous but potentially monetizable model is “prediction markets as media.” Think of all the prediction markets on niche, low-volume, low-likelihood events (Gizan pyramid power generators and Christ’s resurrection come to mind). Arguably the “entertainment/news/cultural value” of these markets could exceed the open interest. How much news coverage could a movement in these markets generate, and what might the estimated economic value of that coverage be? Prediction markets are in effect a probabilistic form of news and media, and it would be exciting to see more designs in that direction. The now-defunct TMR.NEWS comes to mind – this platform enabled people to competitively bet on what they thought tomorrow’s NYT headline would say, and an LLM would judge and award the semantically closest guess. Prediction markets for sports are too pedestrian – maybe we need sports for prediction markets.

Existing prediction markets have no obvious present advantage in building entertainment & media experiences, so we can expect startups to be able to explore this design space as well, though entrepreneurs building in this category will succeed or fail on their ability to make culturally relevant, high-grade consumer experiences.

In Conclusion

Taken together, these dynamics suggest that the most durable opportunities in prediction markets may not lie only in broad consumer event venues themselves, but in the surrounding infrastructure and specialized products that make the category more usable, liquid, and economically durable.

Tower Research Capital began as a high frequency trading firm in 1998, and in the ensuing decades has grown to provide liquidity for most major asset classes across most major liquid venues in the world. Beyond employing expertise in global market microstructure, we build at nearly every level of the tech stack, from abstract modeling down to semiconductor design and data center management. Unlike traditional venture capital firms, Tower Research Ventures is uniquely positioned to provide capital, technical expertise, market insights, and work with ambitious entrepreneurs looking to build what could be the next primitive in financial markets.

Tower Research Ventures would love to speak with entrepreneurs working on a prediction market, a prime broker, a clearinghouse, or ideas we have yet to encounter in the broader prediction markets ecosystem. To get in touch, fill out the form on this page.

If you are interested in this and/or working on something in the prediction market space, please reach out to us at ventures@tower-research.com or pdecio@tower-research.com.

The views expressed herein are solely the views of the author(s), are as of the date they were originally posted, and are not necessarily the views of Tower Research Ventures LLC, or any of its affiliates. They are not intended to provide, and should not be relied upon for, investment advice, nor is any information herein any offer to buy or sell any security or intended as the basis for the purchase or sale of any investment. The information herein has not been and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date of preparation. Certain information contained herein is based on published and unpublished sources. The information has not been independently verified by TRV or its representatives, and the accuracy or completeness of such information is not guaranteed. Your linking to or use of any third-party websites is at your own risk. Tower Research Ventures disclaims any responsibility for the products or services offered or the information contained on any third-party websites.